Microsoft just came out with a private cloud…well, another one. They tried private cloud a few years ago, but quickly moved on to their Azure public cloud service. So far, they have been successful in promoting their public cloud, largely due to their existing customer base. Of course, AWS remains their largest competitor, but Microsoft’s growth has actually accelerated in the IaaS market.

Cloud Storage and Backup Benefits

Protecting your company’s data is critical. Cloud storage with automated backup is scalable, flexible and provides peace of mind. Cobalt Iron’s enterprise-grade backup and recovery solution is known for its hands-free automation and reliability, at a lower cost. Cloud backup that just works.

The larger question: how do the private clouds play within the enterprise? That is a larger question than the viability of Azure Stack. Microsoft is the latest to push private and hybrid cloud, but if they are successful, others are likely to enter, or reenter the market, perhaps even public cloud-only AWS and Google.

Azure Stack has been a long time coming. After a year of technical preview, Microsoft has now delivered the first long-awaited release to its hardware partners. These partners include Dell EMC, HPE, and Lenovo. The partners will begin shipping their integrated systems with Azure Stack in September.

State of Private Cloud

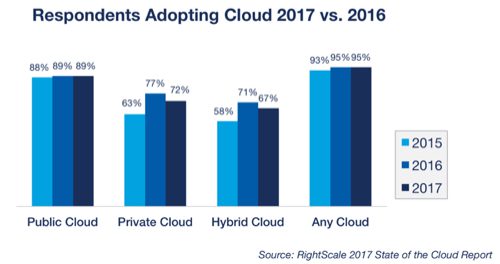

My unscientific opinion is that I don’t see as many private cloud projects out there as a few years ago, but let’s look at the best available data. According to the widely-regarded RightScale state of the cloud report, private cloud has seen a decline in interest. Indeed, as depicted in Figure 1, both private and hybrid cloud (paired public and private clouds), fell a bit in the survey when enterprises were polled about “adopting” specific types of cloud. Public cloud adoption held steady.

RightScale is seeing some reduction in demand for hybrid and private cloud, while public cloud remains steady to growing.

In the same survey, when looking at expanding the use of cloud computing, including migration to the cloud, those citing the expansion of private cloud were dead last. This is relative to a strong interest in 2012 and 2013 as enterprises looked to move to the cloud, but being skeptical around public cloud security and losing control, opted for private cloud platforms.

From the same survey, it was revealed that “Expanding private clouds we use” fell down to last place in 2017.

Looking at these numbers, we see an expanding pattern of decline in both interest and deployment of private and hybrid clouds. Others see this as only a blip. Indeed, there are really no conclusive patterns, if you consider the last 10 years of cloud growth data, including the adoption of private and public clouds.

That said, there are some issues that are arising around the adoption of private clouds. Gartner’s Tom Bittman pointed out in 2015, that there were issues with 95 percent of private cloud deployments, according to a survey Gartner did at one of their conferences. “Focusing on the wrong benefits” was the biggest issue, with enterprises not creating key metrics to measure success or determine failure.

It’s Different Than We Expected

Most of the issues that surround private clouds are really unexpected, when you consider the hype of 10 years ago. Indeed, private clouds were likely a quick invention of traditional enterprise hardware and software providers who wanted to protect their turf, because they viewed public clouds as their market-killers.

These larger enterprise players had access to the hearts and minds of existing enterprise customers who were not glad to see public clouds finally emerge. Public clouds threatened their span of control and forced change in IT shops, where change was typically not wanted. This became the perfect storm of shared interests, and thus private clouds led the cloud computing market, at least, initially.

Reality soon set in. Enterprises that deployed private clouds, such as those based upon OpenStack, CloudStack, VMware, and others, struggled to get the private clouds up-and-running. Or to get any value out of them when they did get them running.

A summary of the complaints was as follows:

First, installation and configuration were complex. Those who implemented OpenStack-based private clouds had trouble getting the open source private cloud installed, tested, and stable. Failed OpenStack implantation projects outnumbered successes 2 to 1, no matter what distribution they selected.

While the more mature private clouds, such as those provide by VMware, seemed to provide better rates of success, they came at a cost that diminished the value that private cloud could bring.

Second, you still buy and own hardware. The promise of cloud computing was the ability to move away from CapEx to OpEx. Private clouds keep you back in CapEx. You can count on purchasing more hardware and software, and with it comes the expense of a data center and people to maintain the hardware and software.

Third, and perhaps the most compelling, the difference in features and functions. Public clouds, by their nature, can continuously expand features. For example, AWS with its “two pizza teams” can add hundreds of services per quarter, or improve the ones that they have.

Let’s say you want lots of different services, the most likely being security services, networking services, database services, governance services, and so on. You can find services in high quantity and quality at the big three public cloud providers. In the private cloud, most of that will be DIY, and some won’t be available at all.

Finally, it’s agility stupid. Private clouds can’t expand or change without some pain, whereas public clouds are better suited to change and expand. It’s a matter of leveraging the utilities model that public clouds leverage, versus the “owned stack” model that private clouds provide. One allows access to thousands of resources on-demand, the other requires that more traditional changes are made to hardware or software that you own and operate.

We’re finding that agility is a much great value provider than operational cost savings. This newly discovered metric continues to emerge as larger enterprises try to figure out the true value of cloud computing. In many cases, agility savings are 10x that of operational cost savings, with public clouds providing the most agility since you have a better ability to provision or change resources than private clouds.

So, Azure Stack?

Given the limitations of private clouds, and the fact that Microsoft has reentered the market, what does the future hold? A few core things are different about Microsoft’s offering.

Azure Stack is really a hybrid cloud sell, and since Microsoft owns the private cloud and public cloud sides of the offering, they can provide tighter integration than the traditional private clouds out there. Other open source private cloud platforms did not have public cloud platform analogs, where Microsoft Azure Stack does…Azure public cloud.

Microsoft typically sells to known customers. The base includes those moving toward Azure and Azure Stack, existing .Net lovers, Office 365 users, and anyone who loves Microsoft everything. This is a huge advantage over Google and AWS who must build a new customer base for public cloud users. Eventually Microsoft will run out of existing customers, and will need to start building a new customer base as well.

Will Microsoft save private clouds for widespread use? Not likely. However, they will save private clouds for their narrow market focus. Or, in other words, they will sell a private cloud that will serve their pubic cloud. Perhaps that’s what existing private cloud solutions were missing.

David Linthicum is SVP at Cloud Technology Partners.

RELATED NEWS AND ANALYSIS

-

Huawei’s AI Update: Things Are Moving Faster Than We Think

FEATURE | By Rob Enderle,

December 04, 2020 -

Keeping Machine Learning Algorithms Honest in the ‘Ethics-First’ Era

ARTIFICIAL INTELLIGENCE | By Guest Author,

November 18, 2020 -

Key Trends in Chatbots and RPA

FEATURE | By Guest Author,

November 10, 2020 -

FEATURE | By Samuel Greengard,

November 05, 2020 -

ARTIFICIAL INTELLIGENCE | By Guest Author,

November 02, 2020 -

How Intel’s Work With Autonomous Cars Could Redefine General Purpose AI

ARTIFICIAL INTELLIGENCE | By Rob Enderle,

October 29, 2020 -

Dell Technologies World: Weaving Together Human And Machine Interaction For AI And Robotics

ARTIFICIAL INTELLIGENCE | By Rob Enderle,

October 23, 2020 -

The Super Moderator, or How IBM Project Debater Could Save Social Media

FEATURE | By Rob Enderle,

October 16, 2020 -

FEATURE | By Cynthia Harvey,

October 07, 2020 -

ARTIFICIAL INTELLIGENCE | By Guest Author,

October 05, 2020 -

CIOs Discuss the Promise of AI and Data Science

FEATURE | By Guest Author,

September 25, 2020 -

Microsoft Is Building An AI Product That Could Predict The Future

FEATURE | By Rob Enderle,

September 25, 2020 -

Top 10 Machine Learning Companies 2020

FEATURE | By Cynthia Harvey,

September 22, 2020 -

NVIDIA and ARM: Massively Changing The AI Landscape

ARTIFICIAL INTELLIGENCE | By Rob Enderle,

September 18, 2020 -

Continuous Intelligence: Expert Discussion [Video and Podcast]

ARTIFICIAL INTELLIGENCE | By James Maguire,

September 14, 2020 -

Artificial Intelligence: Governance and Ethics [Video]

ARTIFICIAL INTELLIGENCE | By James Maguire,

September 13, 2020 -

IBM Watson At The US Open: Showcasing The Power Of A Mature Enterprise-Class AI

FEATURE | By Rob Enderle,

September 11, 2020 -

Artificial Intelligence: Perception vs. Reality

FEATURE | By James Maguire,

September 09, 2020 -

Anticipating The Coming Wave Of AI Enhanced PCs

FEATURE | By Rob Enderle,

September 05, 2020 -

The Critical Nature Of IBM’s NLP (Natural Language Processing) Effort

ARTIFICIAL INTELLIGENCE | By Rob Enderle,

August 14, 2020

CLOUD ARTICLES