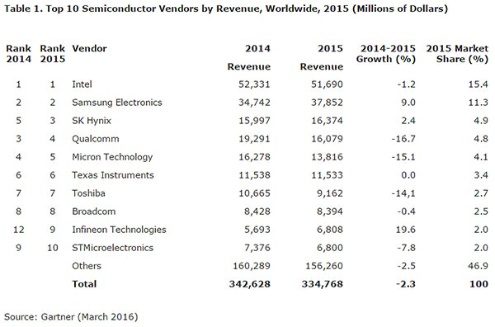

Last year, semiconductor sales fell 2.3 percent to $334.8 billion, according Gartner’s latest analysis of the chip market.

Collectively, the top 25 semiconductor vendor companies, which account for 73.5 percent of the market, experienced a half-percent drop in revenue. The rest suffered a 6.9 percent decline. “The worldwide semiconductor market declined in 2015 as slowing demand for key applications combined with strong currency fluctuations to subdue the market,” observed Gartner research vice president Andrew Norwood.

While changes in demand patterns and various currency moves account for some of the loss, there were other major market forces at play that change the calculus a bit, argued Norwood.

“2015 semiconductor revenue results are skewed by the large amount of M&A activity during the year. If we adjust for this M&A activity by adding in revenue for 2015 and 2014 where necessary, then the performance is somewhat different: The top 25 vendors would have experienced a 1.7 percent revenue decline, and the rest of the market would have declined 3.9 percent,” said Norwood in a statement.

Despite a 1.2 percent drop in revenue, Intel ruled the market in 2015 for the 24th consecutive year with $51.6 billion in chip sales and a 15.4 percent share of market. Second-place Samsung scored a healthy 9 percent jump in sales to $37.8 billion. The Korean electronics giant claimed 11.3 percent of the market in 2015.

Infineon Technologies was another big gainer. The company, known for its industrial and automotive electronics, climbed from twelfth to ninth place last year following a whopping 19.6 percent increase in sales to $6.8 billion.

Nestled in third place is SK Hynix on sales of $16.3 billion and a 4.9 percent share of the market. Fourth-place Qualcomm, a mobile chip maker, saw its fortunes fall 16.7 percent, from $19.2 billion in sales in 2014 to $16 billion last year.

Rounding out the top five is Micron. The memory and flash chip provider experienced a 15.1 percent decline in sales to $13.8 billion.

“2015 saw a mixed performance by the different device categories, unlike 2014 when all categories posted positive growth,” said Norwood. “Non-optical sensors performed best due to increased usage of fingerprint sensors in smartphones, while discretes saw the strongest decline due to a mix of weak demand and currency issues.”

Pedro Hernandez is a contributing editor at Datamation. Follow him on Twitter @ecoINSITE.

RELATED NEWS AND ANALYSIS

-

Huawei’s AI Update: Things Are Moving Faster Than We Think

FEATURE | By Rob Enderle,

December 04, 2020 -

Keeping Machine Learning Algorithms Honest in the ‘Ethics-First’ Era

ARTIFICIAL INTELLIGENCE | By Guest Author,

November 18, 2020 -

Key Trends in Chatbots and RPA

FEATURE | By Guest Author,

November 10, 2020 -

FEATURE | By Samuel Greengard,

November 05, 2020 -

ARTIFICIAL INTELLIGENCE | By Guest Author,

November 02, 2020 -

How Intel’s Work With Autonomous Cars Could Redefine General Purpose AI

ARTIFICIAL INTELLIGENCE | By Rob Enderle,

October 29, 2020 -

Dell Technologies World: Weaving Together Human And Machine Interaction For AI And Robotics

ARTIFICIAL INTELLIGENCE | By Rob Enderle,

October 23, 2020 -

The Super Moderator, or How IBM Project Debater Could Save Social Media

FEATURE | By Rob Enderle,

October 16, 2020 -

FEATURE | By Cynthia Harvey,

October 07, 2020 -

ARTIFICIAL INTELLIGENCE | By Guest Author,

October 05, 2020 -

CIOs Discuss the Promise of AI and Data Science

FEATURE | By Guest Author,

September 25, 2020 -

Microsoft Is Building An AI Product That Could Predict The Future

FEATURE | By Rob Enderle,

September 25, 2020 -

Top 10 Machine Learning Companies 2020

FEATURE | By Cynthia Harvey,

September 22, 2020 -

NVIDIA and ARM: Massively Changing The AI Landscape

ARTIFICIAL INTELLIGENCE | By Rob Enderle,

September 18, 2020 -

Continuous Intelligence: Expert Discussion [Video and Podcast]

ARTIFICIAL INTELLIGENCE | By James Maguire,

September 14, 2020 -

Artificial Intelligence: Governance and Ethics [Video]

ARTIFICIAL INTELLIGENCE | By James Maguire,

September 13, 2020 -

IBM Watson At The US Open: Showcasing The Power Of A Mature Enterprise-Class AI

FEATURE | By Rob Enderle,

September 11, 2020 -

Artificial Intelligence: Perception vs. Reality

FEATURE | By James Maguire,

September 09, 2020 -

Anticipating The Coming Wave Of AI Enhanced PCs

FEATURE | By Rob Enderle,

September 05, 2020 -

The Critical Nature Of IBM’s NLP (Natural Language Processing) Effort

ARTIFICIAL INTELLIGENCE | By Rob Enderle,

August 14, 2020

DATA CENTER ARTICLES